Agricultural market is affected by many factors, both predictable and unpredictable. In the past decade many agribusinesses decided to go organic and others are seriously considering this strategy. One of the first steps of going organic is switching from synthetic to organic fertilisers. To make an informed and profitable decision you need market insights. But there is a ton of data to consider, and conducting your own research is time-consuming and tiresome.

So, we have carefully selected the most important market trends and forecasts and neatly packed them into this article for your convenience.

Key Drivers of Organic Fertiliser Adoption in 2022-2027 and their respective impacts in short-,medium- and long-run

|

Market Drivers |

Short-run Impact in 1-2 years |

Medium-run Impact in 3-4 years |

Long-run Impact in 5 years |

|

Growing consumer demand for organic produce and food |

High |

High |

High |

|

Increasing consumer awareness about ecological benefits of employing organic fertilisers |

Medium |

Medium |

High |

|

Predominant availability of organic waste |

Medium |

Medium |

High |

|

Developments in manufacturing and processing of organic fertilisers |

Medium |

High |

High |

Key Driver Analysis

Unlike synthetic fertilisers, organic ones, including manure and compost, are sustainable, eco-friendly, renewable and biodegradable. They enhance soil structure, improve its water-retention capacity and protect soil and plants from diseases. Also, organic fertilisers are harmless for the environment.

In contrast, synthetic fertilisers leach into the groundwater making it hazardous for soil, animals and people. It's an environmental threat. Another problem is chemical residue in food, which can lead to serious health issues.

Consumers recognised the aforementioned problems and made product safety and eco-friendliness their priorities when choosing produce and food. And scientists agree with them as eating organic is proven to reduce the risk of cancer, heart disease, stroke, obesity and being overweight, and allergic reactions.

Organic farming is being promoted around the world by NGOs, which ask consumers and agribusinesses to pay attention to adverse consequences of chemical residue in food. Governments start legislative initiatives to support organic farming and educate consumers about the benefits of eating organic.

As the world population is forecasted to be 9.8 billion people by 2050, all channels of food production and distribution are vital for future food security. Agriculture was always at the heart of food production and with increasing consumer preference for organic products an increased adoption of organic fertilisers is expected.

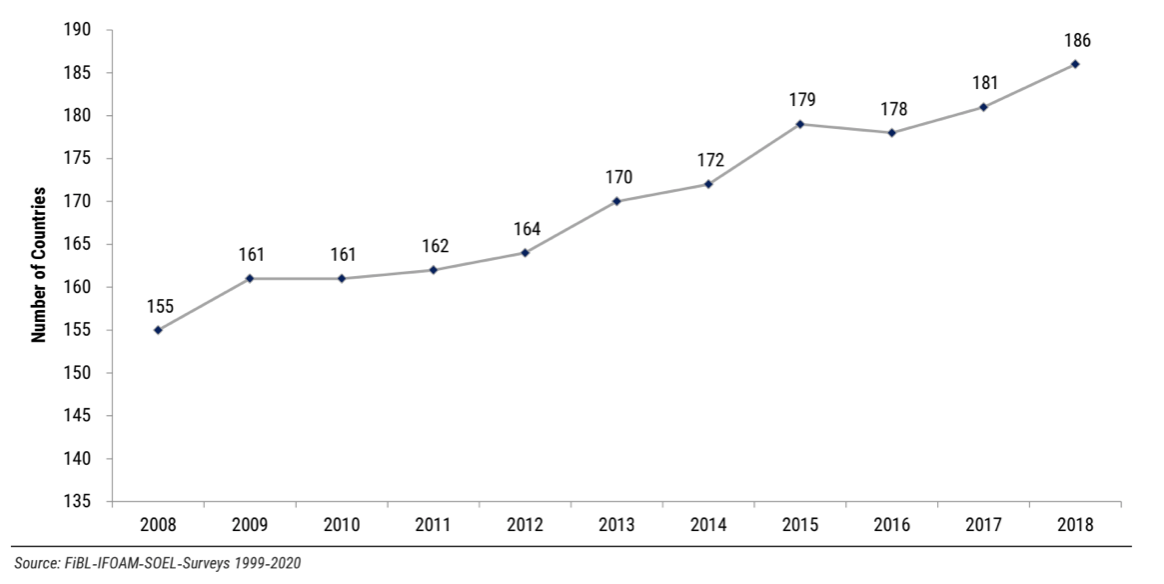

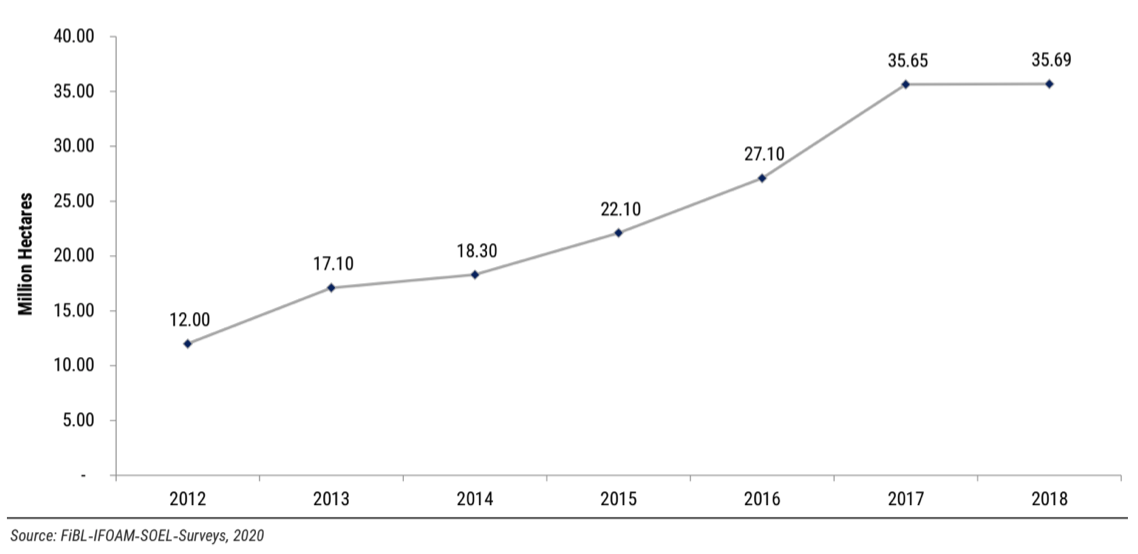

Adoption of Organic Farming by the Number of Countries, 2008–2018

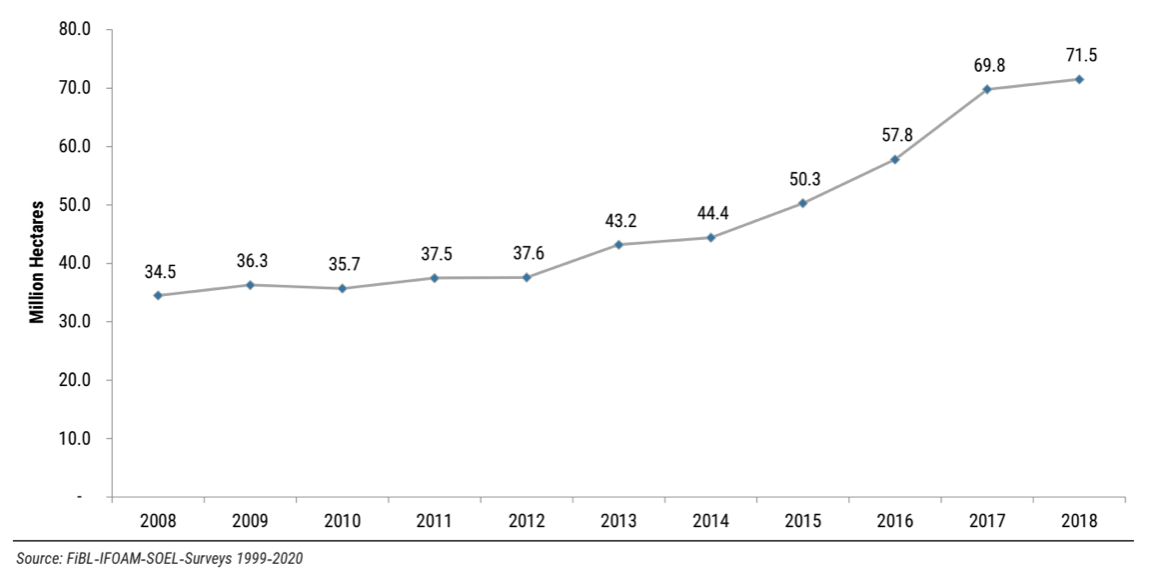

In 2018 organic farming was utilised by approximately 2.8 million farmers in 186 countries and 71.5 mln hectares were farmed organically.

Organically Farmed Land by Hectares

Organically farmed land must be free from synthetic agrochemicals, including artificial nitrogen fertilisers, artificial hormones and GMOs. Organic practises are outlined in governmental policies and special agencies oversee farms which declare they've entered transition to organic farming.

Nonetheless for 10 consecutive years the acreage of organically farmed land was growing and the growth continues today.

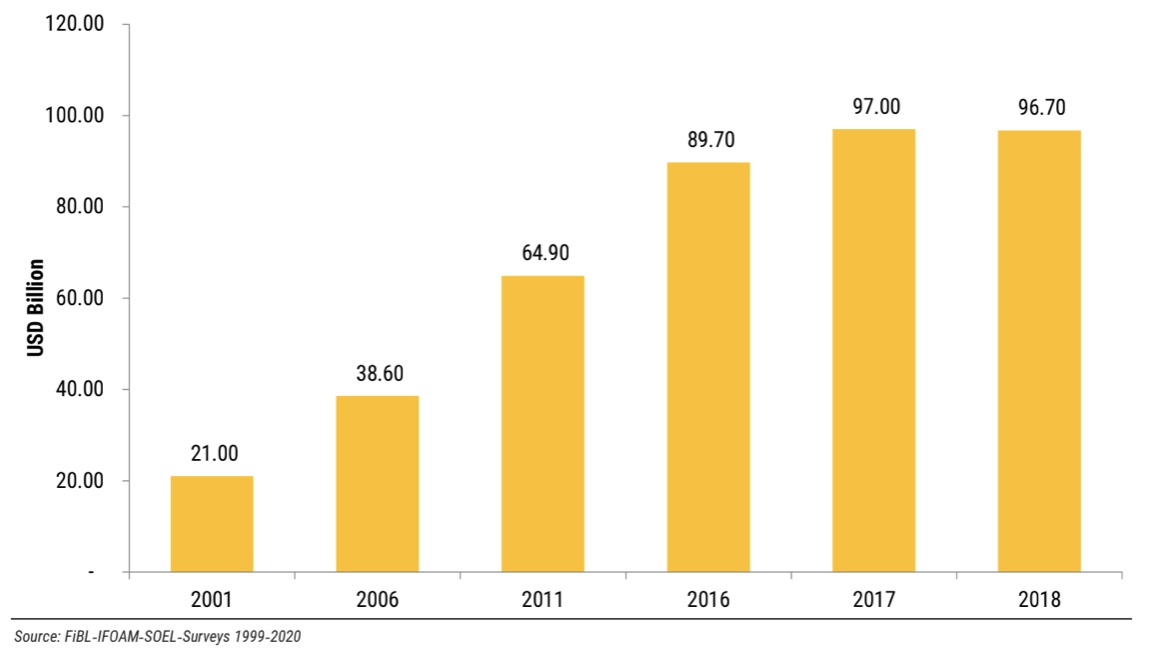

Organic Produce and Food and Drink Market Value measured in sales in USD bln.

Therefore, factors such as the growing need to increase agricultural production, rising awareness about the adverse effects of chemicals on the health and environment, and growing organic area & demand for organic foods are expected to drive the demand for organic fertilisers across the globe.

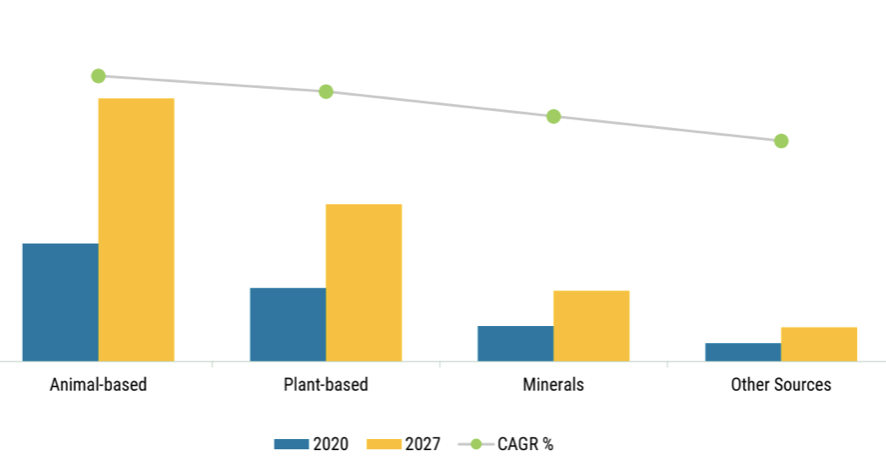

Global Organic Fertiliser Market Segments, – Animal-based, Plant-based, Mineral and Other source, – measured in USD mln. All markets are expected to grow between 2020 and 2027

Animal-based organic fertilisers are expected to remain the largest segment over the forecast period. This type of organic fertiliser is considered very effective due to high levels of nutrients, small time period between application and first results, as well as low dosage required to achieve a desirable outcome. Also, animal waste is readily available on a global scale. However, the vermicompost is a safer and healthier alternative to livestock manure. So not every animal-based fertiliser has the same properties.

Dry and Liquid Organic Fertilisers

Dry organic fertiliser market segment is larger than the liquid organic fertiliser segment both in volume and in value. The difference is created by growing application of dry organic fertilisers for lawns and gardens because of significantly lower risk of plant damage due to slower release of nutrients, as well as long-lasting effect after single use, high level of effectiveness across different climates and easy access to raw materials for production.

Composition of dry organic fertilisers vary from single raw material to a blend of several raw materials. They are known to contain a wide range of nutrients. Specific blends are designed to have a predetermined ratio of different nutrients. Application includes broadcasting, ordinary and band placement and pellet method. Dry organic fertilisers improve soil water-retention, strengthen its structure and increase yield. Yet because these fertilisers are dry and contain particles of varying sizes, they lose in efficiency and absorbability to liquid organic fertilisers.

Compost, ordinary and green manure, bone and feather meal as well as dried blood are usually manufactured as dry fertilisers. In general, their production utilises plant residue and animal waste as raw materials.

That being said, liquid organic fertilisers are forecasted to grow at the highest CAGR between 2022 and 2027. The factors behind such accelerated growth include high level of effectiveness, enhanced penetration of soil and plants, relatively easier application and uniform distribution on any surface and being more cost-effective. Dry organic fertilisers need moisture or irrigation to properly work, so across water scarce areas liquid organic fertilisers are more efficient.

Liquid organic fertilisers produced from vermicompost can be as effective if not more than artificial fertilisers.

Still dry organic fertilisers are expected to retain larger market share than liquid ones in 2027.

Growth of Agricultural and Livestock Production as the Driver of Organic Fertiliser Supply

With population growth the demand for food is constantly increasing. To accommodate the growing demand agricultural and livestock production must step up. However, this kind of production creates billions of tons of inedible residue as a side effect. This residue is ideal for manufacturing dry organic fertilisers and can be easily accessed at slaughterhouses and processing factories. So growth of agricultural and livestock production drives supply of dry organic fertilisers.

Dry Organic Fertilisers by Form of the Content

The main forms of content for dry organic fertilisers are granular, powder and pellet. Other forms of dry organic fertilisers are included into one group called "Other types". By both volume and value the granular segment is the largest.

Granular dry organic fertilisers have an increased shelf life and prolonged nutrient release compared to other types. They are also more effective when applied at pre-plant stages and considered the most convenient for storage.

In developing countries as well as states where farms have lower income, agribusinesses prefer to broadcast granular dry organic fertilisers, including compost and manure. In developed countries agribusinesses prefer mechanical spreading using disk spreaders. Granular organic fertilisers are more suitable for different application methods than other types.

These are the drivers behind demand for granular dry organic fertilisers.

Dry Organic Fertiliser Utilisation by Country

In both volume and value Australia has the largest share of the dry organic fertiliser market. Australia has also the largest share of the granular organic fertiliser market, both in volume and in value.

Organic Fertilisers by Method of Application

Main methods of application include broadcasting, fertigation and foliar application. Remaining ways of application are included in one group named "Other methods". Broadcasting method has the largest market share in terms of volume and is expected to retain the largest share in 2027. The main reasons being affordability, effectiveness and simplicity of this method.

However, the whole market is forecasted to grow with segments like fertigation showing an impressive CAGR between 2022-2027. The drivers behind accelerated growth are:

- Prevalent utilisation of innovative broadcasting equipment and/or machinery, including broadcasters, manure and muck spreaders, honey wagons, centrifugal, boomed and spinner spreaders, aircrafts and unmanned aerial vehicles or UAVs

- Popularisation of advanced irrigation systems

- Increased adoption of fertigation method for organic orchards

- Recognition of this method's benefits, including simplicity and safety of application, maximised absorption by soil and plants, minimum waste of fertiliser, and maximum effectiveness

Methods of Organic Fertiliser Application as Drivers of Organic Farming Practises Adoption

Before going organic farmers consider all risks and benefits. They develop transition strategies that best fit the needs and goals of their agribusiness. And appropriate methods of organic fertiliser application are an integral component of said strategies.

As we've mentioned earlier, broadcasting is one of the most commonly used methods of dry organic fertiliser application. Broadcasting is utilised for fertilising horticultural crops, lawns, gardens and flower beds. This method is generally reserved for insoluble organic fertilisers.

Broadcasting encopasses basal application and top dressing methods. Basal application means uniform distribution of fertiliser across fields and the consecutive mixture of fertiliser with soil. Top dressing application means fertilisers are spread across already growing plants. Prevalent adoption of innovative broadcasting equipment and/or machinery improved uniformity and simplicity of fertiliser distribution across fields. It also made broadcasting methods of application more time- and cost-effective.

That being said, there are downsides to broadcasting, the main being risk of overapplication. If one uses organic fertilisers with high salt content, overapplication may burn the crops. Another downside is fertiliser waste since plant roots cannot fully absorb nutrients when the fertiliser is spread almost horizontally at a large distance from the dispenser. And this is where fertigation methods and foliar application could be more effective. Also, there are organic fertilisers that pass filtration at 80 microns, which excludes clogging of injectors.

Advances in various methods of organic fertiliser application are simplifying the transition to organic practices and making it more affordable.

Dry Organic Fertiliser Method of Application by Country

In terms of both volume and value Australia has the largest share in the broadcasting market segment.

Organic Fertiliser Market by Crop Cultures

The main crop cultures, which are cultivated using organic fertilisers are cereals and grains, fruits and vegetables, oilseeds and pulses, turf and ornaments. Other cultures are included in one category named "Other crops".

Cereals and grains represent the largest market segment among crop cultures cultivated with organic fertilisers, both in terms of volume and value, and are forecasted to retain the largest share in 2027 with the largest CAGR across segments.

The drivers behind these trends include growing consumer demand for organic cereals and grains, as well as the largest acreage allocated to these cultures' cultivation. Also there are factors which positively affect demand for organically cultivated wheat:

- Prevalent utilisation in food production

- Predominant use as animal feed

- Growing usage across different industries, like biofuel production

Wheat production by Volume and by Country

In 2019 over 214 mln. hectares were used for wheat cultivation and wheat yield reached 735+ mln. tonnes. Wheat production worldwide is forecasted to achieve 838 Mt in 2028, with an overall increase of 86 Mt compared to 2018 figure.

Out of 86 Mt increase between 2018 and 2028 the developing countries are expected to account for 45 Mt and the developed countries – for the remaining 41 Mt, with the EU forecasted to have the highest level of wheat production. The cited factors for the EU taking the first place are the quality of grains, competitive prices and high yields.

Among the developing countries India is worth noting, as it ranks third among largest producers of wheat worldwide. By 2028 India is expected to grow wheat production by 15.5 Mt. The drivers behind this growth include:

- Government support via public procurement programme, which ensures stable income for farmers

- Over 95% of cultivated land is irrigated

|

Country or Region |

Forecasted Growth of Wheat Production by 2028 |

|

India |

15.5 Mt |

|

European Union |

13 Mt |

|

Russian Federation |

9 Mt |

|

China |

8 Mt |

|

Ukraine |

6 Mt |

In the Asia-Pacific region China and Kazakhstan represent the largest acreage dedicated to organic wheat cultivation. In 2018 in China 174 thousand hectares were allocated to producing organic wheat, in Kazakhstan – 100 thousand hectares.

Australia has the largest share, both in volume and value, of global organic fertilisers used for wheat cultivation.

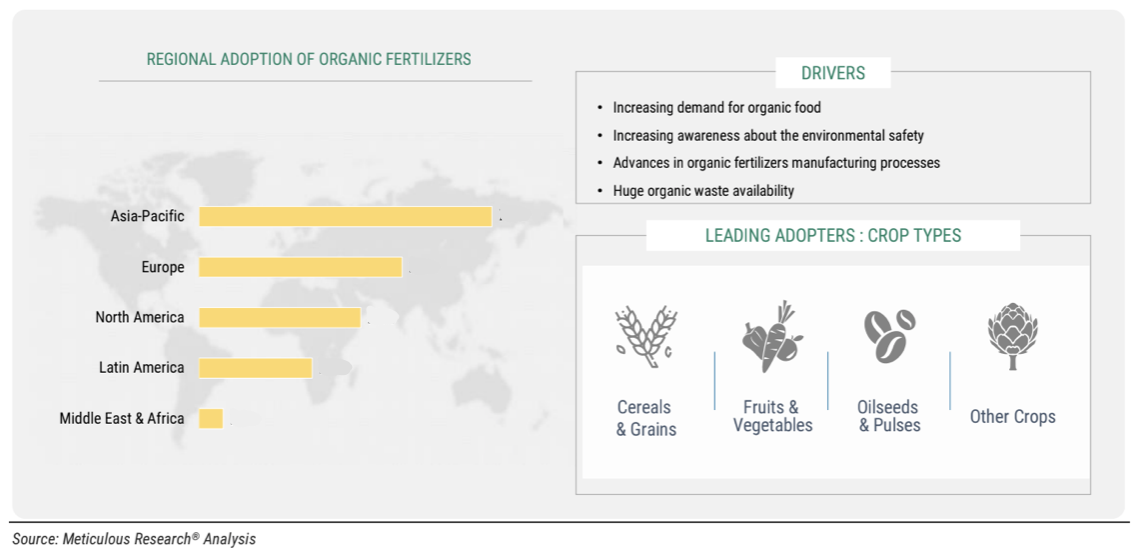

Global Organic Fertiliser Market by Geographic Region

The main geographic regions, where organic fertilisers are applied, are North America, Europe, Asia-Pacific, Latin America, Middle East and Africa.

The largest market share in terms of volume and value belongs to Asia-Pacific and this region is expected to retain the largest share in 2027. The drivers behind the current state of affairs and the forecast are:

- Australia is part of the Asia-Pacific region and it holds and is forecasted to hold in 2027 the largest market shares and expected to retain them for dry organic fertilisers, broadcasting method of application of organic fertilisers, and organic fertilisers used for wheat cultivation

- Largest acreage dedicated to organic farming

- Growing consumer awareness of organic food health benefits

- Growth of population and income

- Growing adoption of irrigation systems and innovative agricultural machinery

- A lot of organic agribusinesses in Asia-Pacific region

- Propagation of legislative initiatives supporting and promoting organic farming

That being said, the highest CAGR between 2022 and 2027 is predicted in North America. Key factors behind this prediction include growing organic food market, increasing consumer demand for organic products and growing acreage dedicated to organic farming.

Already between 2017 and 2018 the global acreage dedicated to organic farming grew substantially:

|

Geographical Region |

Growth of Acreage dedicated to Organic Farming between 2017 and 2018 |

|

Europe |

1.25 mln hectares or 8.7% |

|

Asia |

0.54 mln hectares or 8.9% |

|

North America |

0.1 mln hectares or 3.5% |

|

Oceania |

0.1 mln hectares or 0.3% |

|

Latin America |

13 000 hectares or 0.25% |

|

Africa |

4000 hectares or 0.2% |

Asia-Pacific Region as Key Market for Organic Fertilisers

APAC is considered the most crucial geographical region for both agricultural production and consumption of agriculturally produced commodities. Leading producers on the agricultural market reside in Asia-Pacific and it contains most populated countries across the globe. Over 2.2 bln. residents of APAC rely on agriculture as their primary source of income, including rice growers.

Already in 2018 across Asia over 6.5 mln of hectares were dedicated to organic farming. There were 1.3 mln. organic agribusinesses operating in the region and most of them were located in India. China and India were leading in acreage allocated to organic farming with 3.1 mln. hectares and 1.9 mln hectares, respectively. Seventeen APAC countries already implemented governmental initiatives to support and promote organic farming and eight countries drafted similar legislation in 2018.

By 2019 numerous projects connected to organic agriculture were launched across APAC region, including:

- China enforced third version of National Organic Standard

- In Philippines National Organic Agriculture Board included Participatory Guarantee Systems or PGS into the National Organic Standards

- South Korea launched a pilot project of provision of organic rice to military bases and a government subsidised box scheme of organic food for future mothers

These initiatives are forecasted to accelerate adoption of organic farming practises. As well as rapidly growing demand for organic produce and food across Asia. Whether local agribusinesses can accommodate this growth with an equal supply response remains uncertain. But these trends are forecasted to accelerate consumption of organic fertilisers.

In terms of both volume and value the largest share of the organic fertiliser market in APAC belongs to Australia and this country is predicted to keep the largest share by 2027.

Animal-based organic fertilisers comprise the largest market segment of the APAC organic fertiliser market in terms of value. The segment is predicted to remain the largest by 2027.

Leaders of Organic Fertiliser Market in APAC Region

|

Company |

HQ Location |

|

Suståne Natural Fertiliser Inc. |

USA |

|

The ScottsMiracle-Gro Company |

USA |

|

Beijing Multigrass Formulation Co.Ltd. |

China |

|

Bodisen Biotech Inc. |

China |

|

Qingdao Seawin Biotech Group Co. Ltd. |

China |

|

CityMax AgroChemical |

China |

|

BIOM NZ |

New Zealand |

|

Fertco Limited |

New Zealand |

|

Bennett Fertilisers Limited |

New Zealand |

|

Fertiliser New Zealand Limited |

New Zealand |

|

Plasma Biotec Solutions |

New Zealand |

|

Fertoz Ltd. |

Australia |

|

Qld Organics |

Australia |

|

Biomax Green Australia Pty Ltd. |

Australia |

|

AJ Products |

Australia |

|

FertPro Manufacturing Pty Ltd. |

Australia |

|

Dinofert Fertilisers Pty Ltd. |

Australia |

|

Vitec Organics Pty Ltd. |

Australia |

|

Katek Fertilisers |

Australia |

Australia as a Leader in Production and Consumption of Organic Fertilisers

As you must've noticed, Australia holds and is expected to hold 1st place in 2027 for most segments of organic fertiliser market in terms of market share: dry organic fertilisers, broadcasting method of application of organic fertilisers, organic fertilisers used for wheat cultivation, and organic fertiliser market in APAC.

It's not surprising then that in Australia organic farming has been on a steady rise for the last 42 years. As early as 1980 organic research facilities started to develop strategies for transforming conventional agriculture into organic one. Thus the country became a worldwide leader of organic farming.

Already in 2016 in Australia over 27.1 mln. hectares were allocated to organic farming, which is 5 mln. hectares more than in 2015. Between 2009 and 2019 the acreage dedicated to organic farming in this country increased by over 15 mln. hectares.

Organically Farmed Land in Australia in mln. of hectares

Both farmers and consumers are concerned about using synthetic agrochemicals in food production. Possible contamination and health hazards connected to artificial fertilisers are examples of such concerns, which drive consumer demand for organic food.

And demand for organic food, as well as growth of land farmed organically, drive demand for organic fertilisers. Already in 2015 Australia consumed over 5.3 mln tonnes of organic and inorganic agrochemicals. And the share of organic fertilisers is projected to grow annually.

Many state and private players, including government officials, organic industry groups and representatives of organic supply chains, are actively participating in initiatives designed to increase organic sector value. This drives the rise of the quantity of organic producers, processors and operators.

Number of Organic Producers, Processors and Operators in Australia

|

Year |

Number of Organic Producers, Processors and Operators |

|

2013 |

1700 |

|

2015 |

1829 |

|

2018 |

1876 |

More producers mean larger exports of organic produce and food and continuous growth of Australia's organic produce and food market. Between 2015 and 2016 Australia experienced a 17% growth of organic food export.

A lot of land on the island has naturally inferior soil structure and/or was severely damaged by tillage and overgrazing. Erosion, depletion, low productivity and run-off are common problems for Australian agribusinesses. To restore soil health and improve yields they use large quantities of organic fertilisers.

The aforementioned factors drive demand for organic fertilisers which is forecasted to annually grow in Australia.

Key Players on Australian Organic Fertiliser Market

|

Company |

HQ Location |

|

Suståne Natural Fertiliser Inc. |

USA |

|

The ScottsMiracle-Gro Company |

USA |

|

Odus UK |

UK |

|

M&M Industries/Vivekon |

India |

|

Fertoz Ltd. |

Australia |

|

Qld Organics |

Australia |

|

Biomax Green Australia Pty Ltd. |

Australia |

|

AJ Products |

Australia |

|

FertPro Manufacturing Pty Ltd. |

Australia |

|

Dinofert Fertilisers Pty Ltd. |

Australia |

|

Vitec Organics Pty Ltd. |

Australia |

|

Katek Fertilisers |

Australia |

Australian Organic Fertiliser Market by types of Organic Fertilisers, Methods of Application and Crop Cultures

Animal-based organic fertilisers represent the largest share of the Australian organic fertiliser market, both in terms of volume and value. This segment is predicted to retain the largest shares in 2027.

Blood meal has the largest share of the Australian animal-based organic fertiliser market in terms of value and manure – in terms of volume. Both segments are forecasted to retain the largest respective shares in 2027.

Green manure represents the largest share, both in terms of value and volume, of the Australian plant-based organic fertiliser market and is predicted to retain the largest share in 2027.

Rock phosphate has the largest value and volume shares of the Australian mineral organic fertiliser market. This segment is forecasted to retain the largest shares in 2027.

Dry organic fertilisers represent the largest share in terms of volume and value of the Australian organic fertiliser market. These fertilisers are predicted to retain the largest shares in 2027.

Granular organic fertilisers have the largest share of the Australian dry organic fertiliser market, both in terms of volume and value. These fertilisers are forecasted to retain the largest shares in 2027.

Broadcasting represents the largest, in terms of volume and value, shares in the Australian organic fertiliser market. This segment is predicted to retain the largest shares in 2027.

Cereals and grains have the largest share of the Australian organic fertiliser market, both in terms of volume and value. These crop cultures are forecasted to retain largest shares in 2027.

Wheat represents the largest volume and value shares of the Australian organic cereal and grains fertiliser market. This segment is predicted to retain the largest shares in 2027.

How researchers determined the market size

The volume and value of Organic Fertilisers market was calculated via analysis of market segments. Secondary research determined top market players for each segment. Both primary and secondary research allowed calculation of top players' revenues derived from Organic Fertilisers. Market size estimate is the sum of individual and collective market shares in each segment. The estimate was verified via cross examination against data collected from Key Opinion Leaders or KOLs from the demand and supply side of the market.

How researchers determined segment sizes

During market size calculation the volume and value of source, application, form and crop type segments were calculated. To identify product source, application, form and crop type market shares weight indices were assigned on the basis of source, application, form and crop type utilisation.

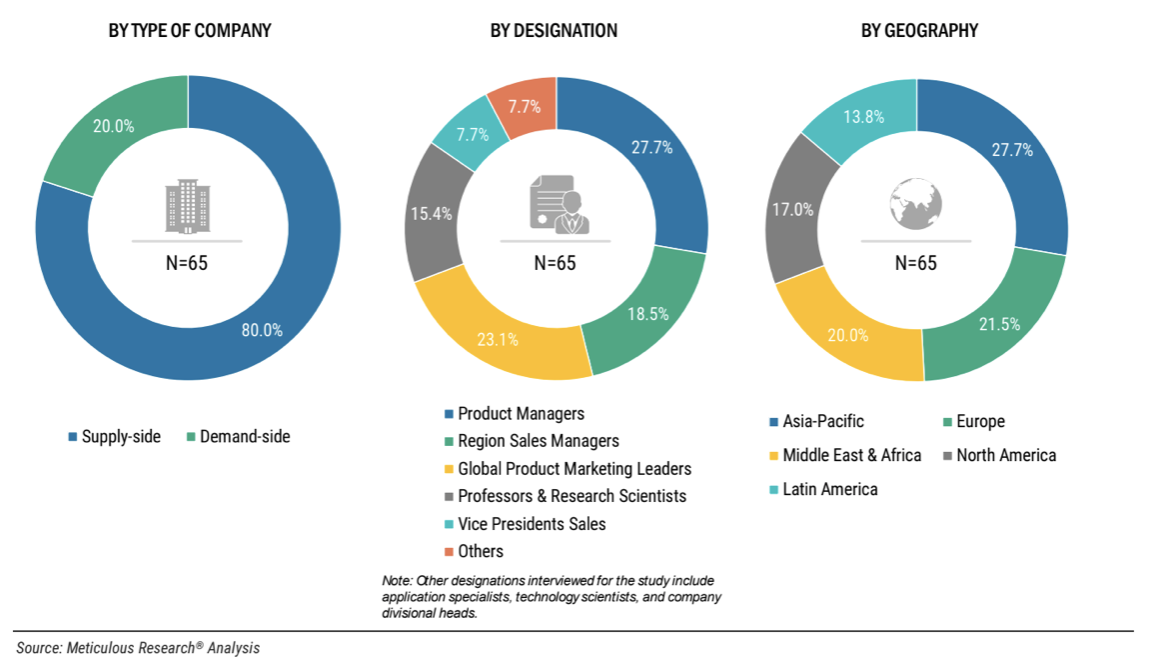

Who participated in the research

Interview quantities and categories on the demand and supply side of the market

How researchers predicted market growth

Researchers conducted a thorough analysis of different quantitative and qualitative indicators, including market leaders' historical revenue growth trends, key growth drivers and limitations and their estimated impacts over the prediction period, as well as relevant macro- and microeconomic factors. They also considered estimated impacts of different strategic developments, including launching new products, establishing new approvals and performing acquisitions.

However, the forecast doesn't take into consideration inflation, recession, changes in currency exchange rates and any sudden regulatory or policy alterations. Unexpected shifts in the global political landscape are also not accounted for. All company records were obtained from the public domain, so any publicly inaccessible statistics, including revenue and changes within the organisation, is not in the scope of this study.

In 2017-2020 several companies dedicated their efforts to obtaining approvals within the international Organic Fertilisers market. Researchers predict that more organisations will seek approvals between 2022 and 2027. They also expect increased adoption of Organic Fertilisers due to consecutive annual growth in the number of agribusinesses, which use these products. Another positive influence is steadily growing demand for organic produce and food. Also, every year China, India, Brazil and other emerging markets introduce new opportunities for organic agribusinesses.

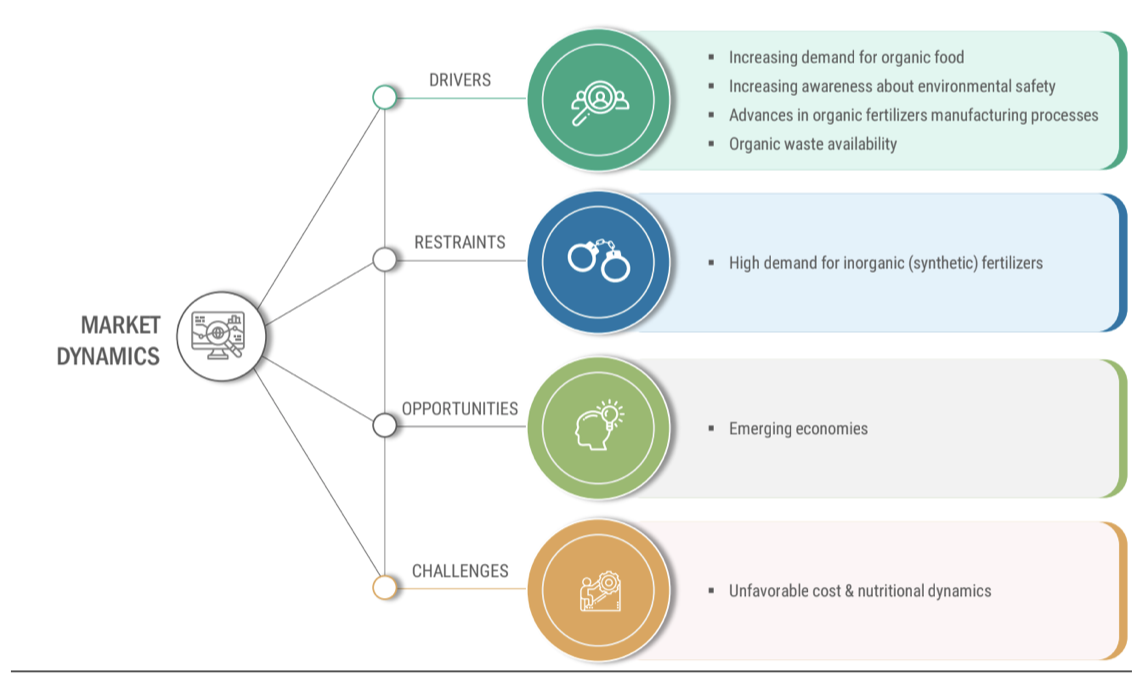

How researchers measured market dynamics

Original Source: Organic Fertilisers Market - Global Opportunity Analysis and Industry Forecasts (2020-2027) – https://www.meticulousresearch.com/enquire-before-buying/cp_id=5135

Learn more about our products

Download a free presentation

Find out how AgroVerm products can help you reduce 30% of your costs

Comments